Published: March 30, 20268 min read

The New NRS Tax Law: How Does It Affect Your Team?

For many employers, the first sign of Nigeria’s new tax regime will not come from a government circular. It will come from employee questions about deductions, take-home pay, and what changed on the payslip.

TL;DR

Nigeria’s new NRS tax law (effective 2025–2026) introduces a restructured tax system, new income tax bands, and clearer rules for deductions and documentation. While the changes may reduce tax for some employees (especially lower-income earners), the real impact will vary based on salary and valid relief claims.

For employers, this is not just a finance issue - it directly affects payroll accuracy, employee trust, and internal coordination. Payroll teams now face higher risk due to stricter rules, while HR must manage employee communication, documentation, and consistency across the organization.

The key takeaway:

Businesses need to update payroll systems, align HR and finance, review employee records, and communicate clearly - because how well you handle tax changes will directly shape employee confidence.

Introduction

For many employers, the first sign of Nigeria’s new tax regime will not come from a government circular. It will come from employee questions about deductions, take-home pay, and what changed on the payslip.

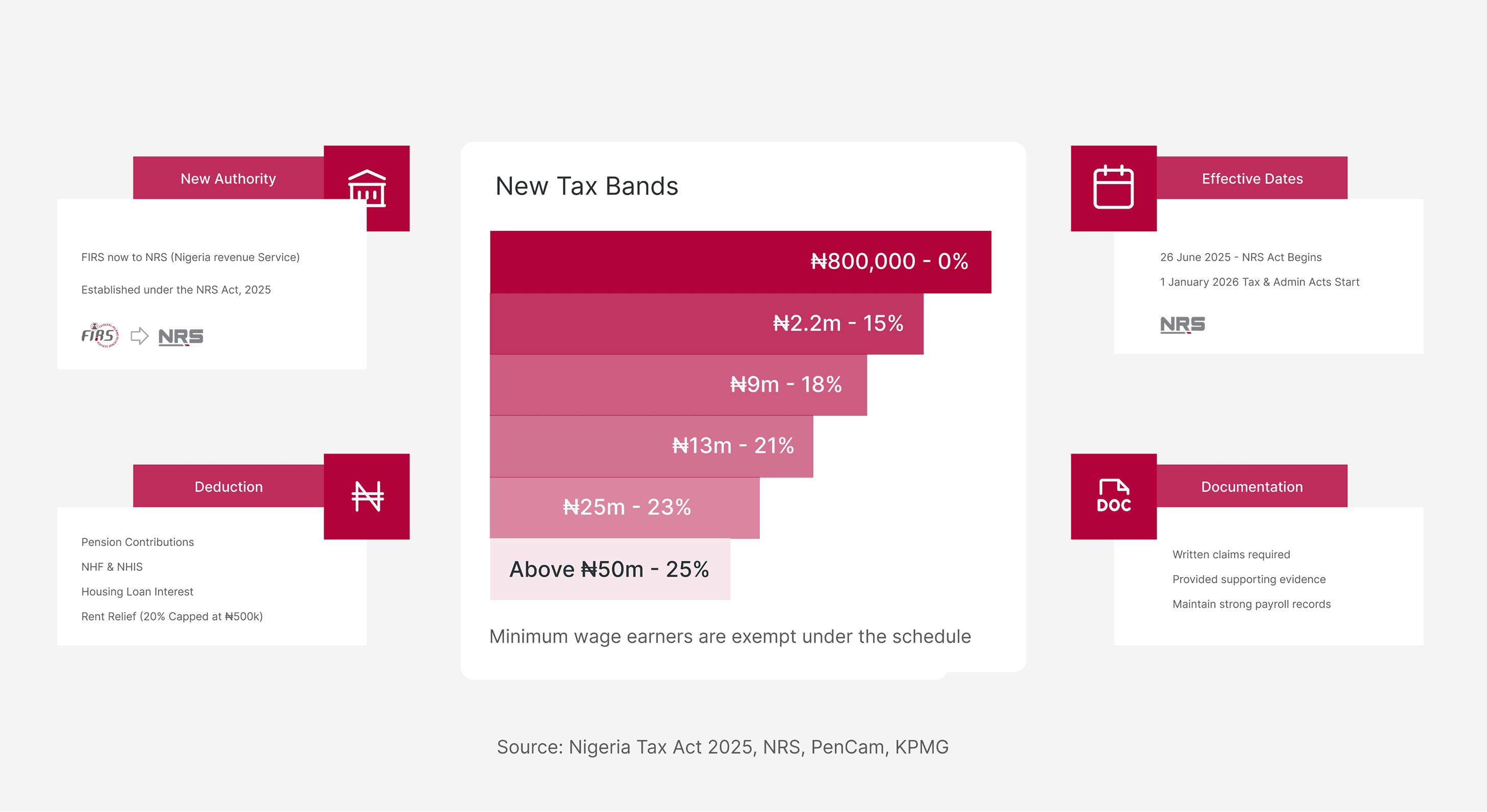

That is why the new NRS tax law deserves attention beyond the tax and finance team. Nigeria now operates under the Nigeria Revenue Service, established by the Nigeria Revenue Service (Establishment) Act, 2025, and the payroll-facing rules now sit within the Nigeria Tax Act 2025. KPMG noted that the Nigeria Tax Act and Nigeria Tax Administration Act became effective on 1 January 2026, while the NRS Establishment Act took effect on 26 June 2025.

For employers, the immediate issue is not whether reform is happening. It is whether payroll, HR, and management processes are ready for the way the reform will show up inside the company.

What Changed Under the New NRS Tax Law?

The structural change is straightforward. The former federal tax authority, FIRS, has been replaced by the Nigeria Revenue Service, backed by a new establishment law. Alongside that institutional change, the Nigeria Tax Act 2025 reorganizes the tax rules into a single framework that covers chargeable income, deductions, rates, administration, and tax treatment across different income categories.

For employers and payroll teams, that “new architecture” matters in three practical ways.First, the law now lays out a revised individual income tax rate schedule under the Fourth Schedule. It taxes the first ₦800,000 at 0%, then applies 15% on the next ₦2.2 million, 18% on the next ₦9 million, 21% on the next ₦13 million, 23% on the next ₦25 million, and 25% above ₦50 million. It also states that an individual earning the national minimum wage is exempt from tax under that schedule.

Second, the law sets out a more explicit framework for allowable deductions and reliefs. Under Section 30, these include qualifying contributions under the pension law, National Housing Fund contributions, National Health Insurance Scheme contributions, interest on loans for an owner-occupied house, some annuity and insurance-related payments, and rent relief of 20% of annual rent paid, capped at ₦500,000.

Third, the law makes documentation and tax treatment more fact-sensitive. It says deductions must be claimed in writing and may be disallowed where satisfactory evidence is not provided. It also sets rules for when employment income is treated as derived from Nigeria, including for some non-resident and cross-border work situations.

So the change is broader than a new tax authority name. The law now gives employers a revised schedule, a revised relief structure, and a clearer documentation burden.

Why Business Owners Should Treat Tax Reform as a Team Issue

Tax reform reaches employees through payslips before it reaches them through policy briefings.

That matters because payroll is one of the few places where leadership decisions become visible in exact numbers. If deductions change and employees do not understand why, management will have questions to answer. If relief is available but handled inconsistently, employees will notice. If payroll teams apply the law unevenly across the workforce, the issue quickly moves from compliance into credibility.

This is why business owners should treat the new tax law as a team issue. Once the law affects what people are paid, what they can claim, and what they must submit to HR or payroll, it becomes part of employee experience.

How the New Tax Rules Could Affect Employee Take-Home Pay

The most obvious employee-level impact is in net pay.

Where the revised tax bands are correctly applied, some lower-income and middle-income employees may see lower personal income tax than before. The exemption for minimum wage earners and the 0% rate on the first ₦800,000 are central here.

But employers should avoid broad internal messaging that suggests everyone will experience the same benefit. The actual payroll effect will depend on salary level, deduction structure, and whether the employee has valid relief claims that the company can process correctly.

That makes communication important. Employees will not only ask whether the law changed. They will ask why their own deduction changed, whether they qualify for relief, and what they need to submit.

Payroll Teams Now Carry More Risk Than Many Employers Realize

The biggest operational pressure point is payroll execution.

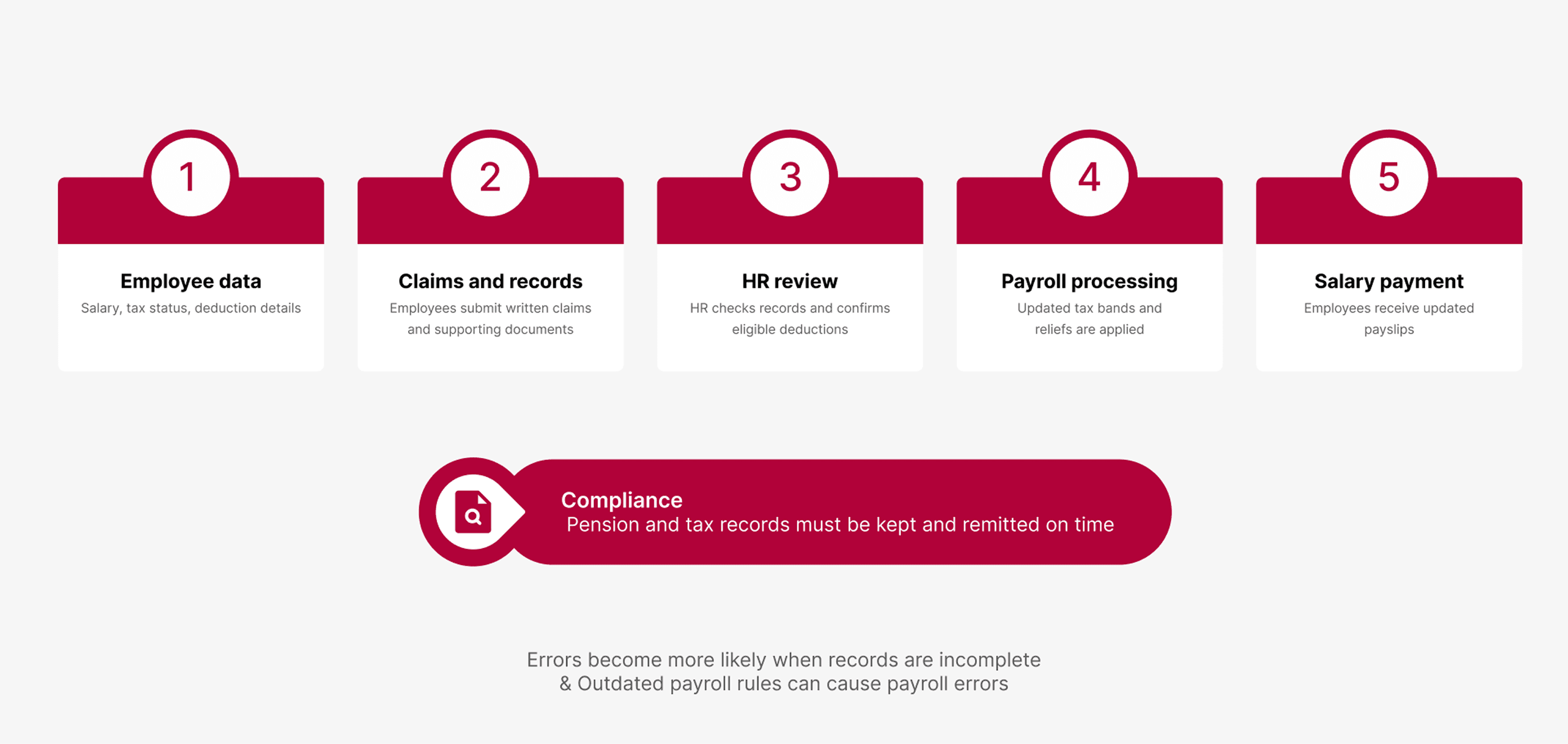

A manual or loosely controlled payroll setup becomes more vulnerable when rate bands change, deduction rules expand, and documentary support becomes more important. Errors in tax deduction create direct employee issues. Delays in pension remittance create regulatory exposure. According to PenCom, employers must remit pension contributions not later than seven working days after salary payment.

For business owners, this means payroll can no longer be treated as a monthly routine that simply needs to “go out on time.” It now requires correct tax logic, complete employee records, and a process for handling claims and supporting documents.

The Real HR Challenge: Communication, Documentation, and Consistency

The tax law creates work for HR even where HR is not responsible for tax interpretation.

If employees want to claim rent relief or other eligible deductions, somebody has to define how those claims will be made, what documents are acceptable, when declarations are due, how records are stored, and how payroll receives final inputs. Section 30 gives the categories. The law’s provisions on written claims and proof determine how seriously employers need to handle the process.

This is where weak internal coordination becomes costly. Finance may understand the deduction rules. HR may hold the employee records. Managers may be the first people employees ask. If those groups are not aligned, the company will create confusion even when it intends to comply.

What This Means for Remote, Cross-Border, and Modern Teams

The law also affects workforce structure.

Section 13 of the Nigeria Tax Act 2025 sets out when employment income is treated as derived from Nigeria. That includes situations involving residence, where duties are performed, whether the employer is Nigerian, whether the income is borne by a Nigerian permanent establishment, and whether the income is taxed in the employee’s country of residence. The same section also provides a carve-out for some non-resident employees working for startups or businesses engaged in technology-driven services or creative arts, where the income is taxable in the employee’s country of residence.

For founders and CEOs, this means remote and cross-border hiring decisions now require closer tax review. A single payroll assumption cannot be applied across all worker categories without checking the facts.

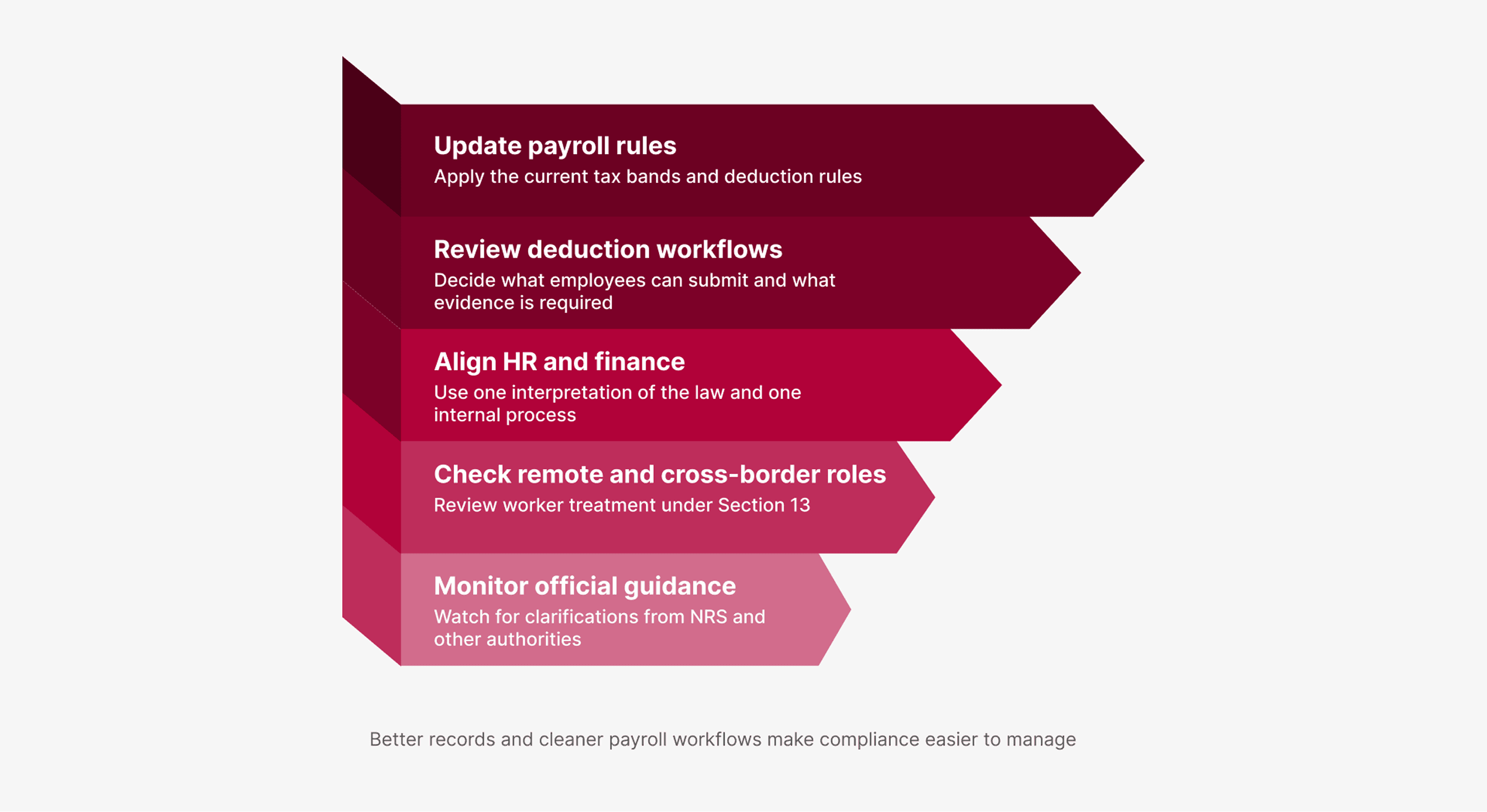

What Employers Should Do Now

The first step is to review payroll configuration against the current rate schedule and the current deduction rules in the Nigeria Tax Act 2025.

The second is to audit what employee declarations and supporting documents the company currently collects, especially where those records affect taxable income.The third is to align finance, HR, and leadership on one internal interpretation before employees start asking questions.

The fourth is to revisit remote and cross-border worker treatment in light of the law’s source-of-income rules.The fifth is to stay close to updates. KPMG’s January 2026 review highlighted errors, inconsistencies, gaps and omissions in the new tax laws, which means further clarifications may still shape employer practice.

Final Thought: Tax Readiness Now Shapes Employee Confidence

Employers that handle this change well will rely on accurate payroll, cleaner records, and stronger communication between HR and finance. That is where Workstat fits naturally. As payroll rules become more detailed and employee data matters more, businesses need a system that helps them keep records organized, workflows consistent, and payroll execution easier to manage.

Employee Management Made Easy

Manage employees and records in one place

Track attendance and manage leave requests

Run payroll and monitor performance seamlessly